The implications of the difference between facts and knowledge

Should organisations make decisions that are based on facts, or on knowledge? A recent paper1 reflects on the difference between facts and knowledge and the implications of this in the context of fraud investigations.

There is a growing private industry in the area of fraud examinations consisting of global auditing firms, local law firms, and independent detectives. Their task is to reconstruct past events and sequences of events related to potential misconduct and crime in the client organization.

The paper authors alert that as causality is difficult to establish, it seems tempting to some fraud examiners to enter into a blame game to make sure that they draw conclusions from investigations that clients have paid for. When facts remain facts, then the blame game can easily occur. A misleading conclusion can be the consequence of failing to transform facts into knowledge, which the authors define as the combination of facts, interpretation, context, and reflection.

Further, even when a private investigator transforms facts into knowledge by a process of interpretation, context inclusion, and personal reflection, the result might still be a misleading or wrong conclusion. The authors advise that this is because providing sense to facts require a basic understanding of the relevant knowledge area:

If attorneys from a law firm conduct an investigation, then their knowledge might be insufficient when it comes to accounting figures and organizational structures. If certified public accountants from an auditing firm conduct and investigation, then their knowledge might be insufficient when it comes to the psychology and sociology of executive deviance. If a former homicide detective is to study the crime scene, then documents and computers rather than bodies and blood are relevant to understand

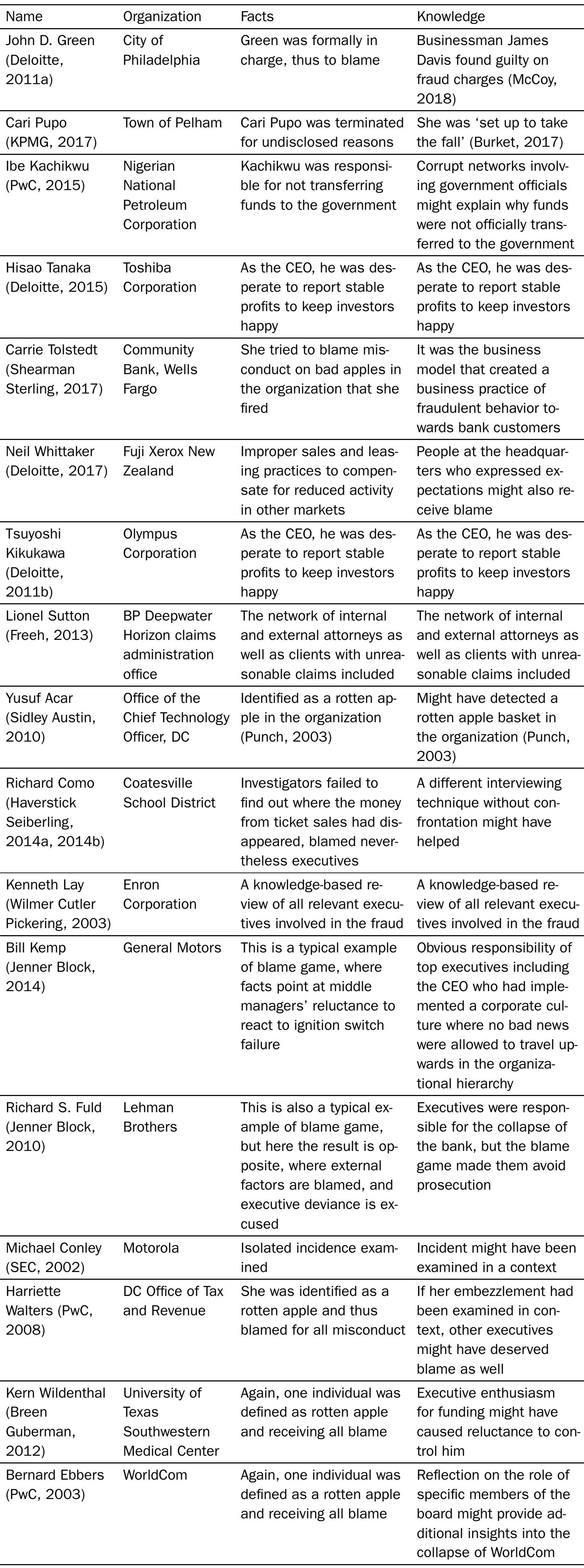

To illustrate their arguments, the authors present a facts versus knowledge perspective for a sample of 17 investigation reports by fraud examiners (Table 1).

As the knowledge perspective in Table 1 shows, the difference between facts and knowledge is all the more reason for organisations to engage in knowledge management.

Article source: Facts or Knowledge? A Review of Private Internal Reports of Investigations by Fraud Examiners is licensed under CC BY-NC-ND 4.0.

Image source: mohamed_hassan on Pixabay, Public Domain.

Reference:

- Gottschalk, P. (2018). Facts or knowledge? A Review of private internal reports of investigations by Fraud examiners. International Journal of Management, Knowledge and Learning, 7(2), 165–185. ↩

Also published on Medium.