There are several contributing factors that played a part in Silicon Valley Bank’s (SVB) demise. In short, less stringent regulatory requirements of midsized or ‘regional’ US banks allowed SVB to build a massive loss-making bond portfolio which had to be prematurely liquidated, at a significant loss, to service $42 billion worth of panic withdrawals in only a few days.

What is Silicon Valley Bank?

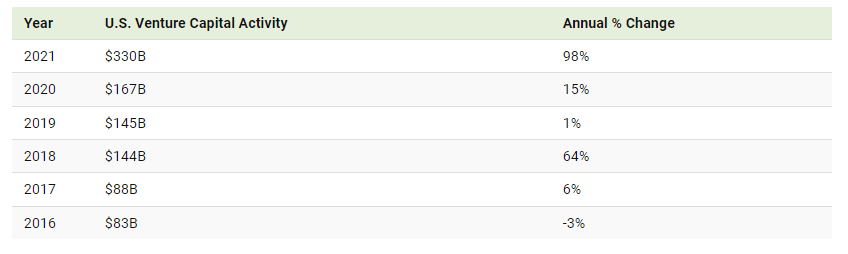

Silicon Valley Bank is a midsized US bank headquartered in California that served as a pillar for the venture capital (VC) and start-up community during the tech boom of 2019-2022. The bank offered traditional banking services but had a large concentration of its client base in one sector – the rapidly growing technology sector. In 2021, venture-capital backed companies amassed a monumental $330 billion – twice what was raised in 2020 – as low interest rates provided access to cheap money.

Source: Pitchbook, Visual Capitalist

Furthermore, the massive amounts of funding for tech start-ups meant that the percentage of total deposits in excess of the FDIC insured amount of $250,000 in the event of a bank failure, was around 90%. The $250,000 limit is applied on a per customer basis offering little piece of mind for massive depositors. Essentially, all of this meant that only 10% of deposited funds would be fully recovered in the event of the failure of SVB, exposing the majority of its clients to financial ruin.

Rapid Rise, Even Faster Decline

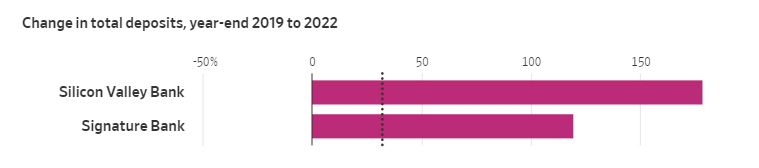

Silicon Valley Bank benefitted from the rise in VC-backed funding and its depositor base rose three-fold between 2020 and 2022. To give you an idea of how rapidly depositors flocked to SVB, the chart below reveals that over the same period, the industry average, while impressive, showed only a 32% increase in the aggregate deposit base (dotted vertical line).

Source: Wall Street Journal

The reopening of the global economy after global lockdowns, near-zero interest rates, along with an influx of monetary stimulus from the Federal Reserve Bank created the ideal backdrop for investors looking for more attractive alternatives to low yielding bonds and cash. As such, the riskier, high growth tech sector took off. Well, at least until the Federal Reserve reversed course and started hiking interest rates at break-neck speed to contain rampant inflation. This was the very same inflation brought about, in part, by the extremely loose monetary conditions created by the Fed in the first place.

Bank Run: What Caused the Mass Withdrawals?

Multiple events over the course of a few days set in motion one of the fastest snowballing effects that ultimately led to SVB’s collapse.

Ratings Agency Moody’s Downgrades SVB Credit to ‘Negative’

SVB realised a $1.8 billion loss after the bank was forced to sell part of a $21 billion loss-making portfolio to raise enough cash to meet increasing customer withdrawals. The bank had made an ill-informed and reckless bet that the Fed would keep interest rates low and thus, when the Fed hiked aggressively SVB’s unrealized bond losses soared. Interest rates and bonds have an inverse relationship which means as interest rates rose, bond prices fell, resulting in the massive loss-making bond portfolio.

This caught the attention of one of the major rating’s agencies, Moody’s, which subsequently downgraded SVB’ credit rating. In response, the company announced its intention to raise $2.25 billion in fresh capital by selling new shares, which didn’t go down well with the market. The sheer size of SVB’s illiquid ‘held-to-maturity’ investments (poorly performing bond portfolio) spooked depositors who realized it would be near impossible to liquidate the sizeable holdings into cash to meet withdrawals in the event of a run on the bank.

Mass Media Coverage Ensues as Money Managers Advise Clients to Withdraw Deposits

Once the media got hold of the story, investors became jittery, and withdrawals increased. To make things worse, large money managers like Peter Thiel’s Founders Fund, advised companies to withdraw funds held with SVB.

Source: SKY

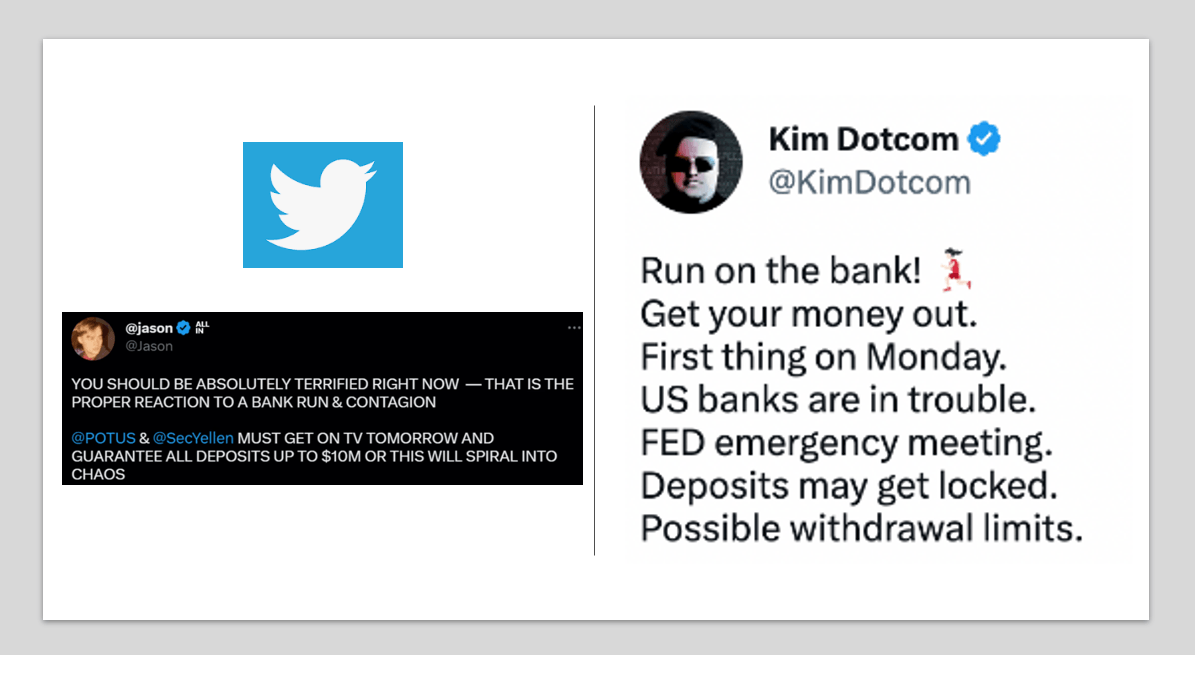

World’s First Twitter-Fuelled Bank Run

Withdrawal requests rose exponentially, aided by advances in technology which facilitates withdrawals with just a few clicks of a mouse, largely in contrast with bank runs of the past which could be identified by massive lines of worried customers outside regional bank branches. Twitter also helped spread the panic as influential people in the tech/start-up space like Jason Calacanis and Kim Dotcom weighed in on the increasing likelihood of a bank run.

Source: Twitter

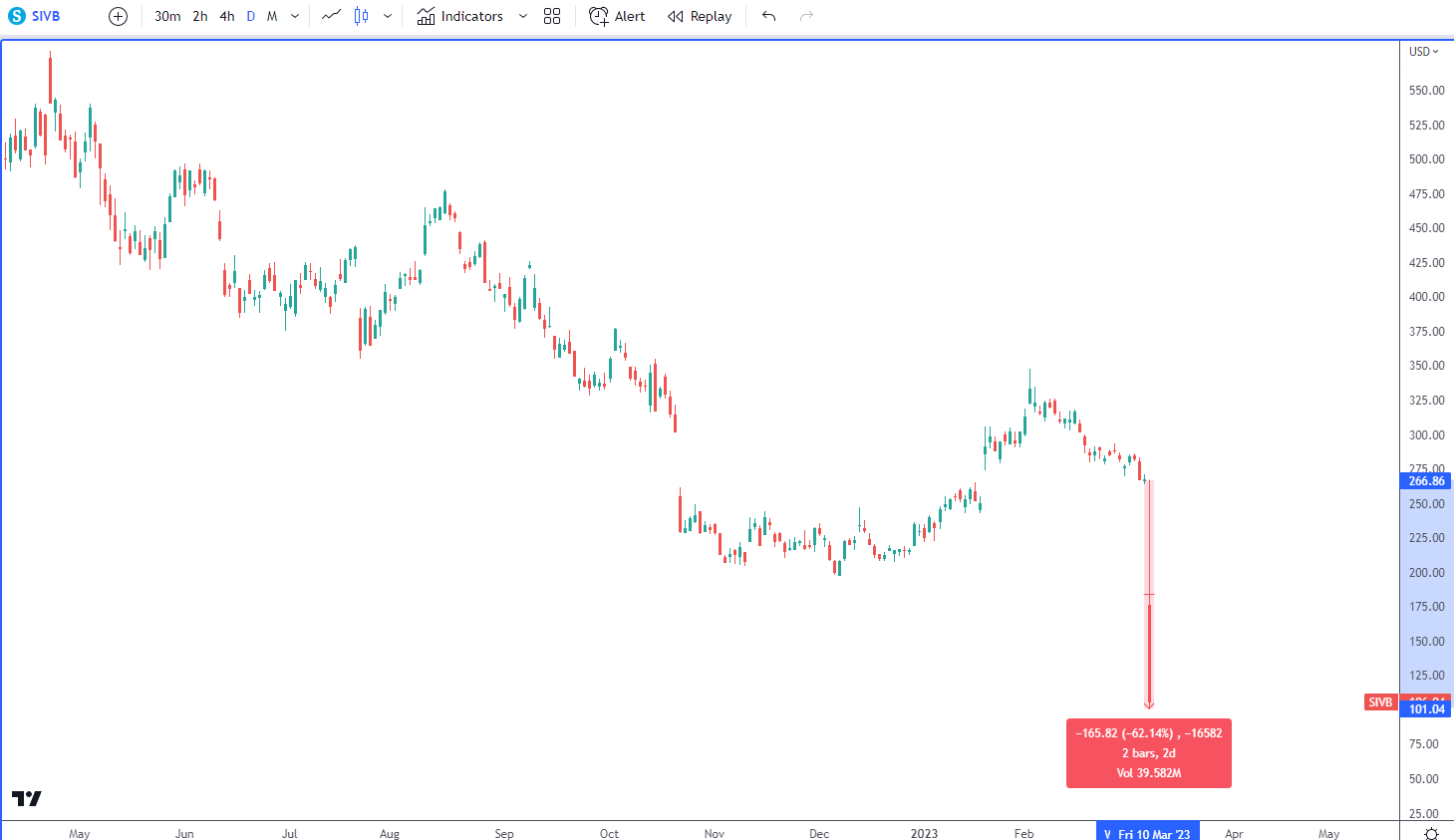

“SVB” was tweeted around 200,000 times on Thursday the 9th of March as several founders and tech CEOs posted about withdrawing money from the bank. Large scale panic set in and customers demanded around $42 billion worth of withdrawals on the same day as faith in the bank’s ability to meet withdrawals diminished by the minute. SVB’s share price lost roughly 60% in after-hours trading.

SVB Share Price (Daily Chart)

Source: Tradingview

The Fallout from SVB’s Collapse and Potential Contagion Effect

SVB’s failure brought with it the demise of Signature Bank – a favourite banking institution for the crypto industry – and Silvergate Bank, and left another regional financial institution, First Republic Bank, requiring massive amounts of credit and financial backing from household banks to shore up confidence.

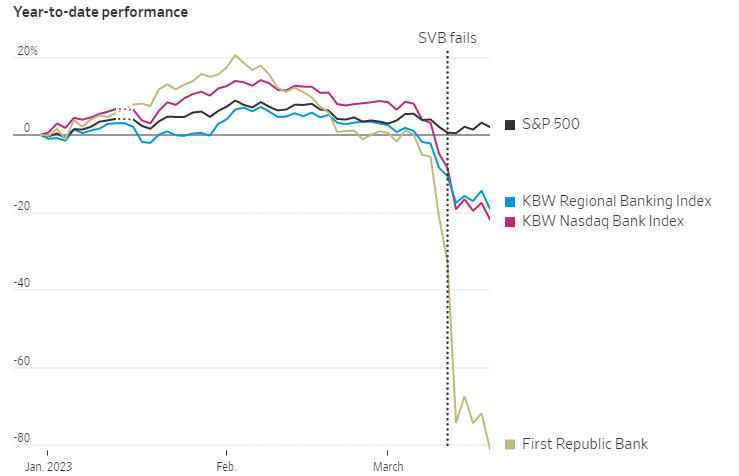

Source: Wall Street Journal

Further afield, the already tainted reputation of Credit Suisse meant that the Swiss lender represented the weakest link in the European banking system, threatening a large-scale capitulation if it hadn’t been for the decisive action of the Swiss National Bank to force through a sale to its local competitor, UBS. Only time will tell if the worst is behind us.

US banking indices remain rooted around recent lows as confidence in the sector is yet to be revived. In addition, the reality of continued elevated interest rates suggest that banks will have their work cut out for them. Whether that arises in the form of a further loss of confidence or a deteriorating loan book as mortgage defaults are likely to pick up, remains to be seen.